Is this part of loan rip off that hurts middle-class & poor?

It seems that the poor and the struggling middle-class simply cannot get a break. Income inequality and wealth disparity are real. We are now hearing politicians talk a lot about it. They speak about it as if it is something that happened in a vacuum that they are now interested in solving.

What politicians never do is accept the reality, the responsibility they hold for creating a framework that allowed the pilfer of the poor and the middle class. The every day incentives and actions that most of us see and sometimes disregard are the very things that continue to promote the pilfer. The following loan rip off is a classic example.

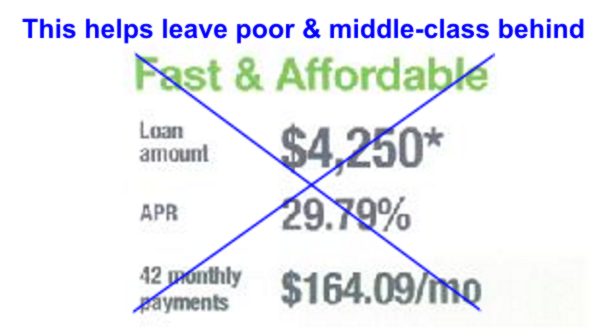

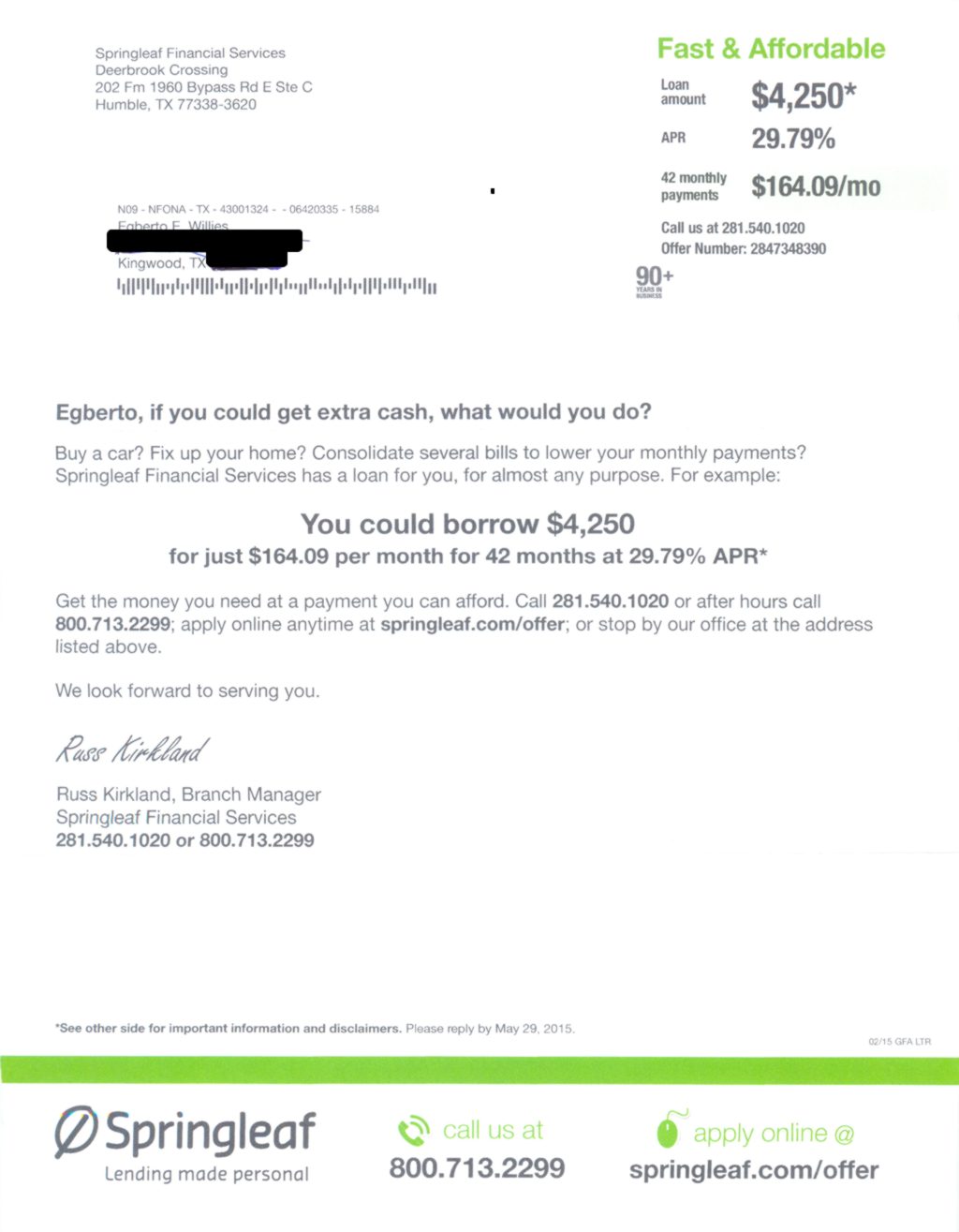

I received the following piece of mail this weekend. My blood began to boil. Is this an example of a legal loan rip off of the poor & middle-class? In my opinion it is.

I am posting this as a public service. But I am also posting it because of my memories of the disadvantage I had to overcome when forming my software company on 21% consumer credit while ‘others’ had the ability to form their companies with 6% loans. Our system continues to pilfer the poor, a section of the middle-class, and the systematically oppressed.

To be clear, I am virtually debt free sans mortgage, short term business loan, and a liquid line. As such, it is evident that this was likely a wide net mail-out fishing for those that may be at a low point and in need of a slight temporary cash flow lift. As a full time blogger and activist, like many other middle-class and poor folk, it is not difficult to envision a time when during an emergency or a cash flow slump, this could become an only option. It can happen to us all.

New regulations forced corporations providing loans to be more transparent. In the past it is likely this invitation for a ridiculously high priced loan rip off (29.79% APR) would have just included the amount and seemingly affordable monthly payment without the Annual Percentage Rate (APR) or duration of the loan displayed. The information is now there and as such it is legal.

For all those who think regulations are burdensome and slows down business, they are right. Business should feel a regulatory burden when their impact could be detrimental to society, the function of society, or life itself. Should we not have regulations that insulate citizens from a pilfer when they have their backs against the wall with virtually no choices or options? We should all be empathetic no matter our current status in society. A long lasting functioning society depends on it.